Beneath the Strait

Iran could threaten Persian Gulf data centers, undersea cables

By Masha Kotkin

Former energy advisor at US Department of State

By Barbara Slavin

Distinguished fellow at the Stimson Center

The United Arab Emirates, Saudi Arabia, Qatar, and other Persian Gulf countries view investment in artificial intelligence (AI) and IT services as a path to creating a highly skilled workforce and diversifying from oil and gas extraction.

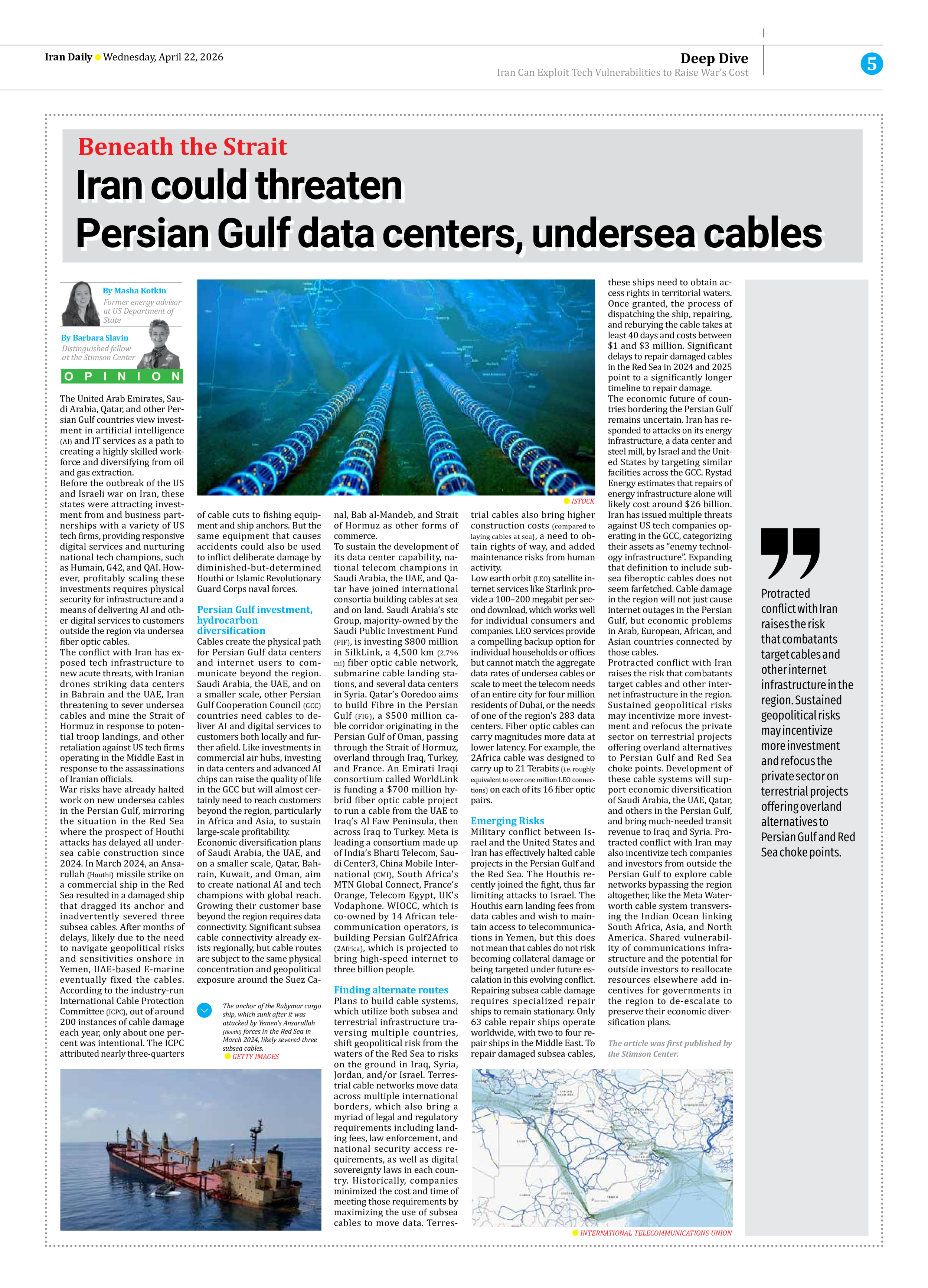

Before the outbreak of the US and Israeli war on Iran, these states were attracting investment from and business partnerships with a variety of US tech firms, providing responsive digital services and nurturing national tech champions, such as Humain, G42, and QAI. However, profitably scaling these investments requires physical security for infrastructure and a means of delivering AI and other digital services to customers outside the region via undersea fiber optic cables.

The conflict with Iran has exposed tech infrastructure to new acute threats, with Iranian drones striking data centers in Bahrain and the UAE, Iran threatening to sever undersea cables and mine the Strait of Hormuz in response to potential troop landings, and other retaliation against US tech firms operating in the Middle East in response to the assassinations of Iranian officials.

War risks have already halted work on new undersea cables in the Persian Gulf, mirroring the situation in the Red Sea where the prospect of Houthi attacks has delayed all undersea cable construction since 2024. In March 2024, an Ansarullah (Houthi) missile strike on a commercial ship in the Red Sea resulted in a damaged ship that dragged its anchor and inadvertently severed three subsea cables. After months of delays, likely due to the need to navigate geopolitical risks and sensitivities onshore in Yemen, UAE-based E-marine eventually fixed the cables. According to the industry-run International Cable Protection Committee (ICPC), out of around 200 instances of cable damage each year, only about one percent was intentional. The ICPC attributed nearly three-quarters of cable cuts to fishing equipment and ship anchors. But the same equipment that causes accidents could also be used to inflict deliberate damage by diminished-but-determined Houthi or Islamic Revolutionary Guard Corps naval forces.

Persian Gulf investment, hydrocarbon diversification

Cables create the physical path for Persian Gulf data centers and internet users to communicate beyond the region. Saudi Arabia, the UAE, and on a smaller scale, other Persian Gulf Cooperation Council (GCC) countries need cables to deliver AI and digital services to customers both locally and further afield. Like investments in commercial air hubs, investing in data centers and advanced AI chips can raise the quality of life in the GCC but will almost certainly need to reach customers beyond the region, particularly in Africa and Asia, to sustain large-scale profitability.

Economic diversification plans of Saudi Arabia, the UAE, and on a smaller scale, Qatar, Bahrain, Kuwait, and Oman, aim to create national AI and tech champions with global reach. Growing their customer base beyond the region requires data connectivity. Significant subsea cable connectivity already exists regionally, but cable routes are subject to the same physical concentration and geopolitical exposure around the Suez Canal, Bab al-Mandeb, and Strait of Hormuz as other forms of commerce.

To sustain the development of its data center capability, national telecom champions in Saudi Arabia, the UAE, and Qatar have joined international consortia building cables at sea and on land. Saudi Arabia’s stc Group, majority-owned by the Saudi Public Investment Fund (PIF), is investing $800 million in SilkLink, a 4,500 km (2,796 mi) fiber optic cable network, submarine cable landing stations, and several data centers in Syria. Qatar’s Ooredoo aims to build Fibre in the Persian Gulf (FIG), a $500 million cable corridor originating in the Persian Gulf of Oman, passing through the Strait of Hormuz, overland through Iraq, Turkey, and France. An Emirati Iraqi consortium called WorldLink is funding a $700 million hybrid fiber optic cable project to run a cable from the UAE to Iraq’s Al Faw Peninsula, then across Iraq to Turkey. Meta is leading a consortium made up of India’s Bharti Telecom, Saudi Center3, China Mobile International (CMI), South Africa’s MTN Global Connect, France’s Orange, Telecom Egypt, UK’s Vodaphone. WIOCC, which is co-owned by 14 African telecommunication operators, is building Persian Gulf2Africa (2Africa), which is projected to bring high-speed internet to three billion people.

Finding alternate routes

Plans to build cable systems, which utilize both subsea and terrestrial infrastructure traversing multiple countries, shift geopolitical risk from the waters of the Red Sea to risks on the ground in Iraq, Syria, Jordan, and/or Israel. Terrestrial cable networks move data across multiple international borders, which also bring a myriad of legal and regulatory requirements including landing fees, law enforcement, and national security access requirements, as well as digital sovereignty laws in each country. Historically, companies minimized the cost and time of meeting those requirements by maximizing the use of subsea cables to move data. Terrestrial cables also bring higher construction costs (compared to laying cables at sea), a need to obtain rights of way, and added maintenance risks from human activity.

Low earth orbit (LEO) satellite internet services like Starlink provide a 100–200 megabit per second download, which works well for individual consumers and companies. LEO services provide a compelling backup option for individual households or offices but cannot match the aggregate data rates of undersea cables or scale to meet the telecom needs of an entire city for four million residents of Dubai, or the needs of one of the region’s 283 data centers. Fiber optic cables can carry magnitudes more data at lower latency. For example, the 2Africa cable was designed to carry up to 21 Terabits (i.e. roughly equivalent to over one million LEO connections) on each of its 16 fiber optic pairs.

Emerging Risks

Military conflict between Israel and the United States and Iran has effectively halted cable projects in the Persian Gulf and the Red Sea. The Houthis recently joined the fight, thus far limiting attacks to Israel. The Houthis earn landing fees from data cables and wish to maintain access to telecommunications in Yemen, but this does not mean that cables do not risk becoming collateral damage or being targeted under future escalation in this evolving conflict. Repairing subsea cable damage requires specialized repair ships to remain stationary. Only 63 cable repair ships operate worldwide, with two to four repair ships in the Middle East. To repair damaged subsea cables, these ships need to obtain access rights in territorial waters. Once granted, the process of dispatching the ship, repairing, and reburying the cable takes at least 40 days and costs between $1 and $3 million. Significant delays to repair damaged cables in the Red Sea in 2024 and 2025 point to a significantly longer timeline to repair damage.

The economic future of countries bordering the Persian Gulf remains uncertain. Iran has responded to attacks on its energy infrastructure, a data center and steel mill, by Israel and the United States by targeting similar facilities across the GCC. Rystad Energy estimates that repairs of energy infrastructure alone will likely cost around $26 billion. Iran has issued multiple threats against US tech companies operating in the GCC, categorizing their assets as “enemy technology infrastructure”. Expanding that definition to include subsea fiberoptic cables does not seem farfetched. Cable damage in the region will not just cause internet outages in the Persian Gulf, but economic problems in Arab, European, African, and Asian countries connected by those cables.

Protracted conflict with Iran raises the risk that combatants target cables and other internet infrastructure in the region. Sustained geopolitical risks may incentivize more investment and refocus the private sector on terrestrial projects offering overland alternatives to Persian Gulf and Red Sea choke points. Development of these cable systems will support economic diversification of Saudi Arabia, the UAE, Qatar, and others in the Persian Gulf, and bring much-needed transit revenue to Iraq and Syria. Protracted conflict with Iran may also incentivize tech companies and investors from outside the Persian Gulf to explore cable networks bypassing the region altogether, like the Meta Waterworth cable system transversing the Indian Ocean linking South Africa, Asia, and North America. Shared vulnerability of communications infrastructure and the potential for outside investors to reallocate resources elsewhere add incentives for governments in the region to de-escalate to preserve their economic diversification plans.

The article was first published by the Stimson Center.